Deregulation And Sectoral Restructuring Gave Rise To Innovation

GP1 discussed the fact that Australian agriculture was still adjusting to the post-deregulation era. For decades, almost all major Australian agricultural commodities had been subject to some form of regulation.

Regulation included single desk selling to export markets, subsidised minimum-price purchasing of commodities by governments and regional restrictions within Australia as to where products could be sold.

Common globally, these structures were aimed at maximising the effectiveness of marketing Australia’s exports, as well as maintaining the viability of domestic farmers.

In the decades leading up to GP1 being published, Australian governments took the controversial decision to gradually dismantle each of these structures. This was primarily for economic reasons, as the cost of government intervention in the market was deemed unsustainable. This decision was also in line with a wide range of changes being made across many Australian industries at the time. Governments of all persuasions were seeking to allow industries, including agriculture, to become more efficient. In addition, as global trade agreements and rules became more prominent, deregulation increasingly became a necessary change to grant access to certain markets.

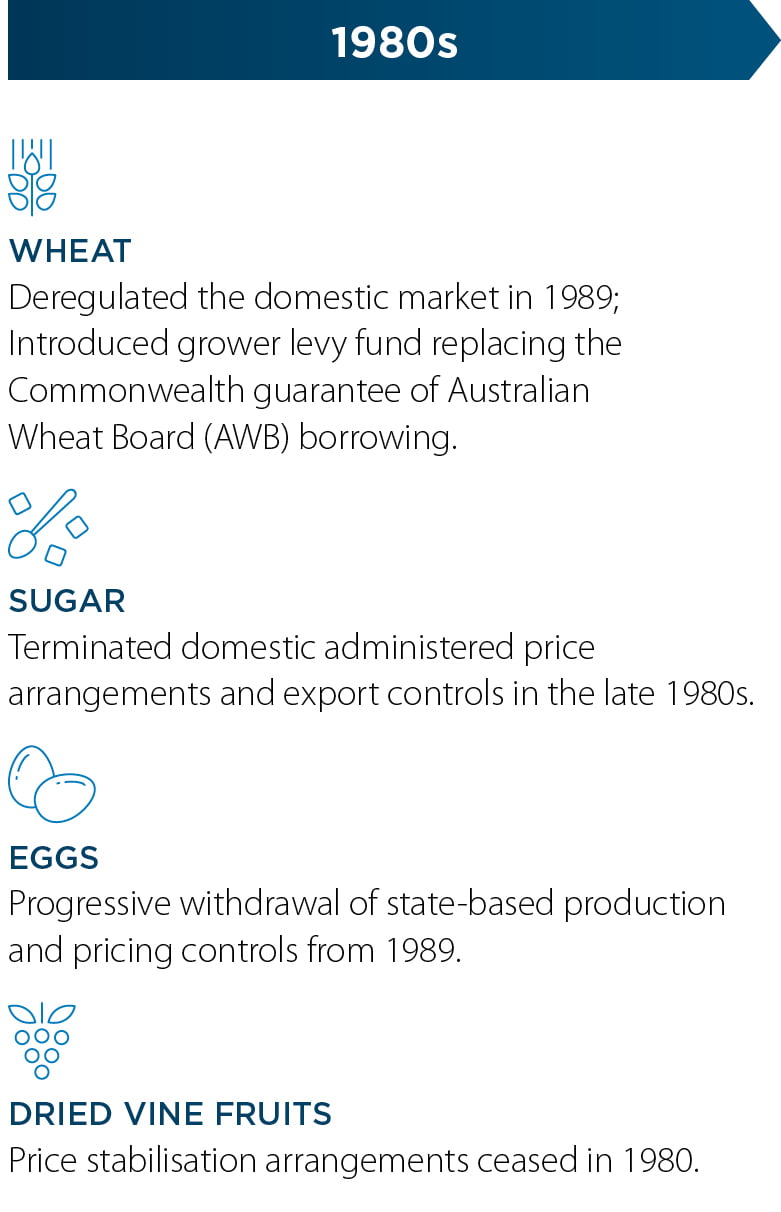

Different commodity regulations changed at varying speed. While the Wool Reserve Price Scheme finished in 1991, the last of the wool stockpile wasn’t sold until 2001.

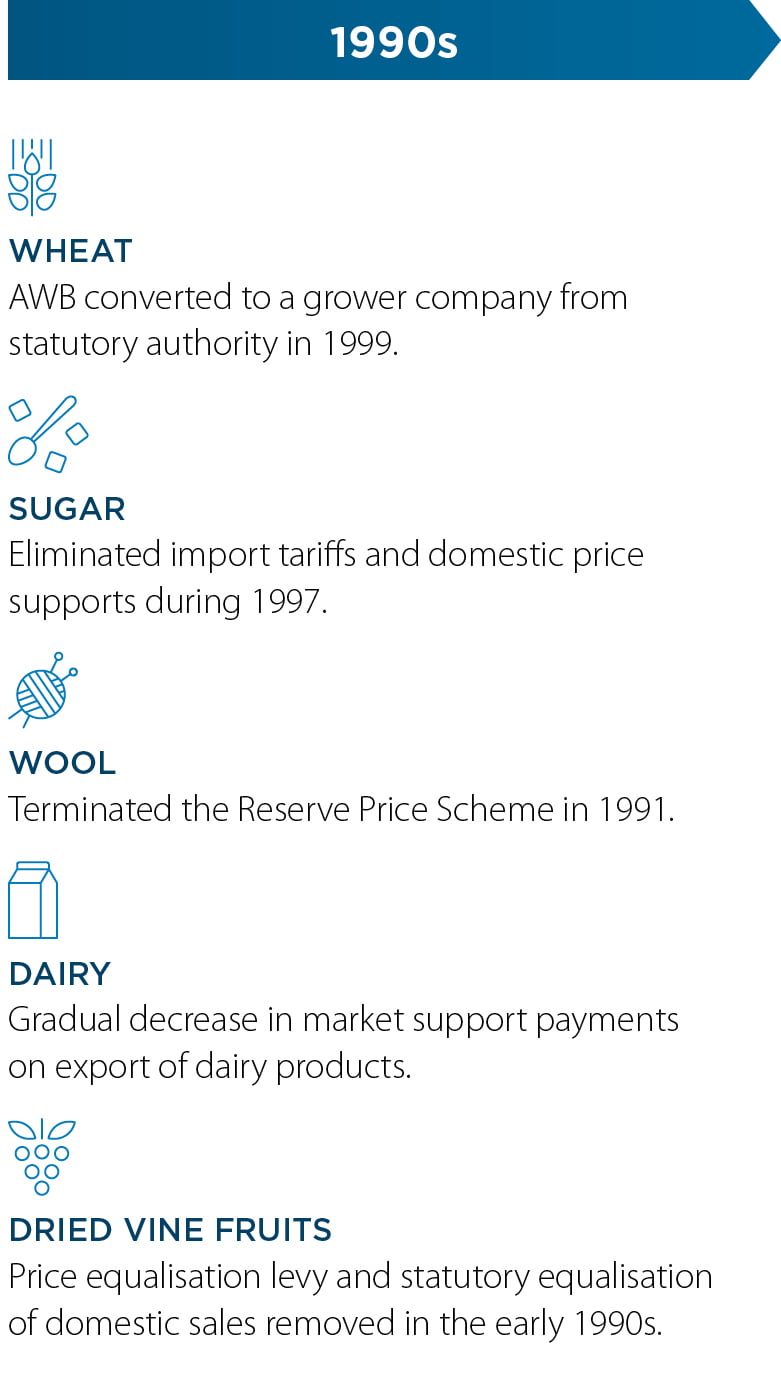

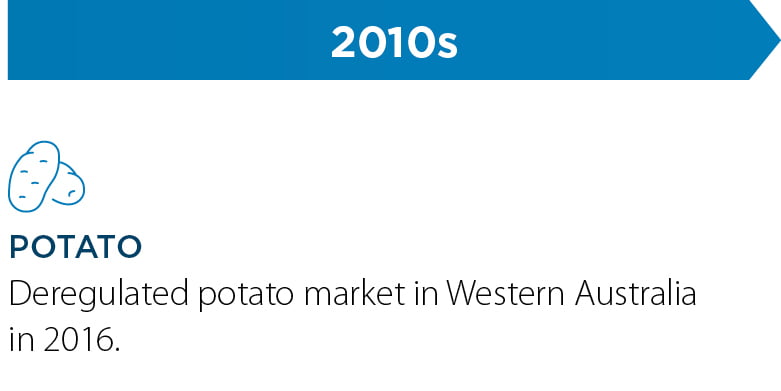

Australia’s dairy industry, which had previously observed state border restrictions, was deregulated in 2000, while the wheat single desk scheme was finally abolished in 2008. Subsequently, sectors including barley and sugar have also emerged from single desk structures. The most recent deregulation was the potato market in Western Australia in 2016.

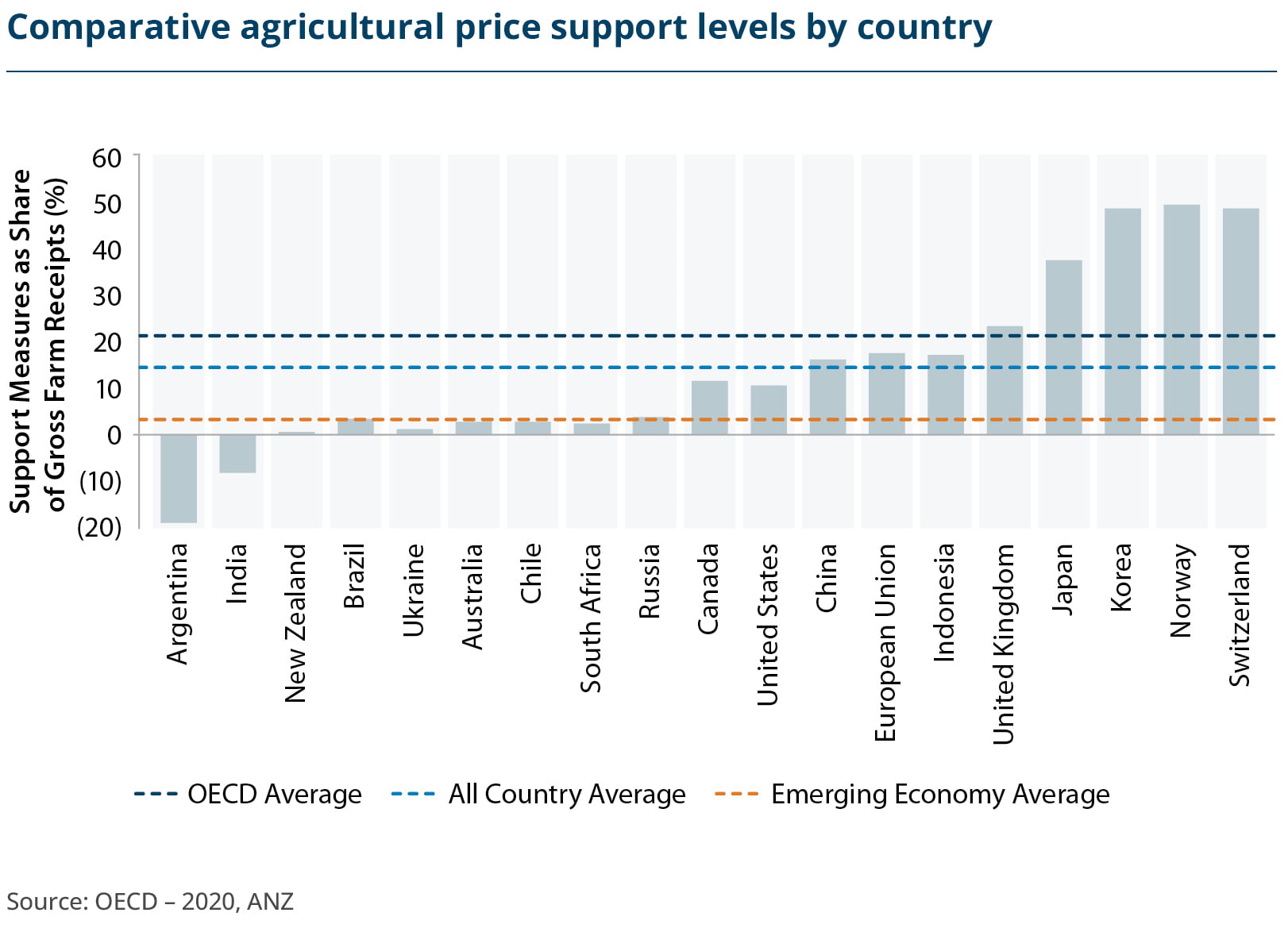

Looking toward 2030, the need for some forms of industry regulation remains the subject of debate in a number of agriculture sectors. Supporters of this argument highlight issues such as declining producer and production volumes in some industries – dairy being a major example – as well as the ongoing subsidy programs enjoyed by most of Australia’s major agriculture export competitors. The debate around the need for greater water regulation has also remained consistently strong.

The freedom to choose marketing outlets for their commodities as well as pursue individual trade relationships has enabled modern producers to explore innovative developments tailored to their buyers’ needs.

While the global discussion centres around agricultural subsidies – and whether some of Australia’s major competitors should look to reduce them – the situation remains that for domestic political reasons in many countries, little is likely to change. This is a reality with which Australian agriculture must come to terms.

This development has ultimately created an environment where innovative players down the supply chain have the potential to flourish unimpeded.

The freedom to choose marketing outlets for their commodities as well as pursue individual trade relationships has enabled modern producers to explore innovative developments tailored to their buyers’ needs. An impressive example of this can be seen in the innovations made by some of Australia’s largest grain producers, to tailor their products specifically to the needs of their export partners.

The ability for producers to select between exporters has further provided them with the opportunity to enhance their returns and build their business, benefitting the overall strength of the sector.

Further along the supply chain, the rise of new marketing bodies has not only facilitated entry into fresh markets for Australian agricultural products but also led to improved efficiency across logistics and distribution networks.

As the process of farm consolidation evolves, and as both corporate and family farms continue to grow in both their sophistication and their global outlook, the benefits of deregulation will continue to provide further benefits to the industry in the years to come.