Australian Agriculture’s Capital Requirements Eventuated

In the space of a decade, the discussion around investment in Australian agriculture has experienced a fundamental shift. Ten years ago, the debate largely revolved around two major points – whether the level of investment required by the industry could be raised, and what the balance should be between domestic and foreign investment.

Looking ahead to 2030, the agricultural investment discussion has changed focus to two quite separate questions – on which agricultural sectors should investment be focused, and how efficiently can the current investment inflows be deployed.

When looking into the issue of investment in agriculture, it is important to remember that this topic stretches broadly across a range of definitions. The most widely discussed focus is on foreign direct investment (FDI), under which capital from outside Australia is invested in the domestic agricultural sector.

It is also important to remember that a large component of agricultural investment comes through reinvestment by those already in the system. This includes retained earnings through profitability, as well as debt through earnings and balance sheet strength, particularly through land values.

At the time, GP1 discussed the potential for debt capping, raising the likelihood that investment would need to come from outside the farming operations themselves.

Ultimately, over the period of 2010–2020, debt played a larger role than had been anticipated. As the decade played out and despite the droughts experienced through that time, farm profitability and balance sheet strength also improved beyond initial forecasts.

A decade on, while these questions remain important ones to ask, it is the responses to them that have changed. This change shows how far Australian agriculture has come over the past 10 years, and also signals the challenges for the future.

GP1 based its forecasts for capital requirements on the volume of agricultural production which Australia would require to fulfill forecast export needs. These export requirements were based on the forecast demand growth of Australia’s export markets.

The modelling separated the capital requirements into two parts:

Capital required to increase production and efficiency on farms, supply chains and infrastructure.

Capital required to buy out farms, largely as a result of generational change.

The increased production forecasts were based on a continuation of the growth trends of Australia’s agricultural output, feeding into both the domestic and export markets, while farm turnover forecasts were based on recorded farm transactions leading up to that period.

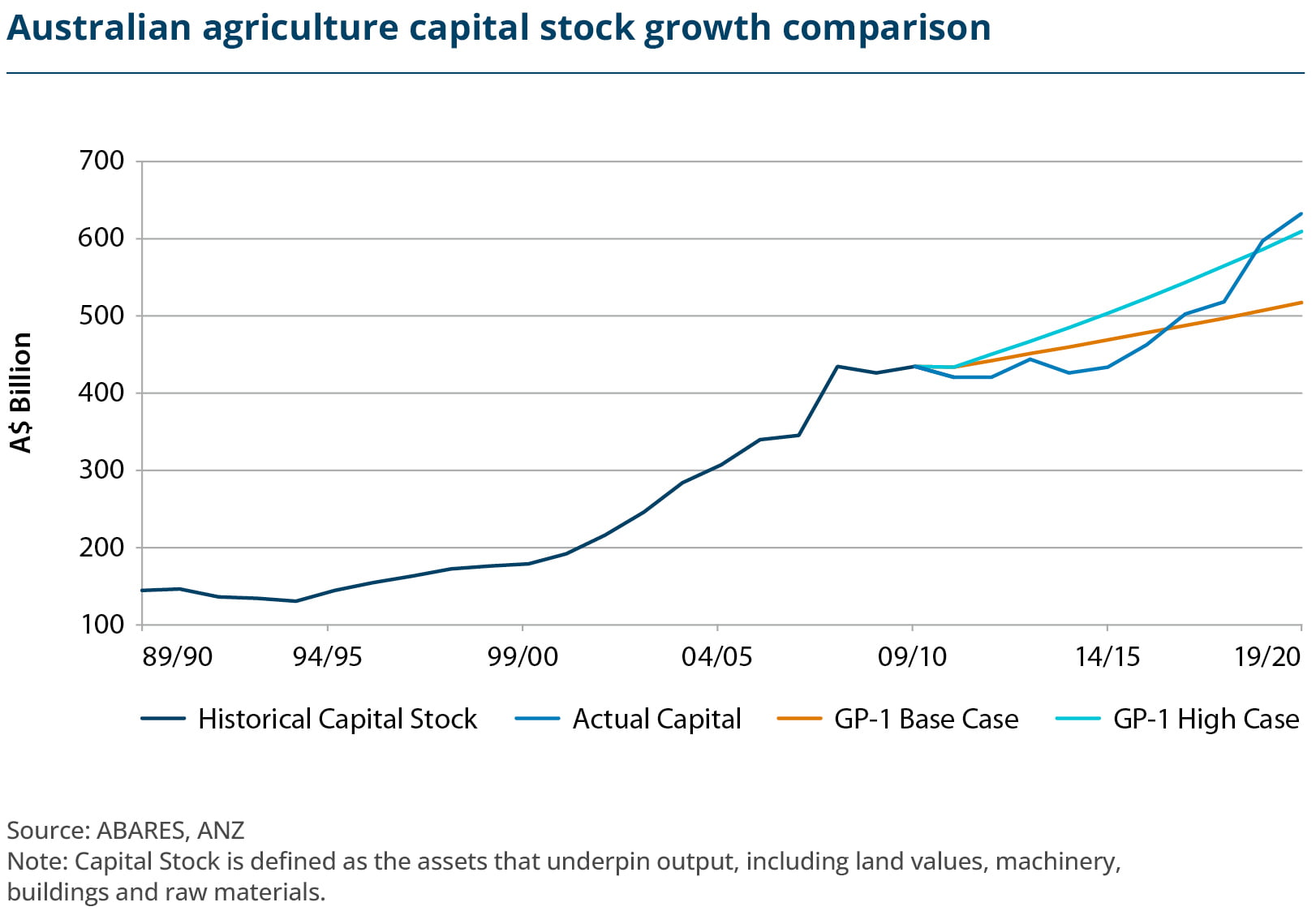

GP1 forecast that for agriculture to grow at the base case (as distinct from the low and high case scenarios) between 2010 and 2050, the industry would require an additional $600 billion in investment for capital improvement and $400 billion for farm turnover.

For the decade of the 2010s, this translated as Australia requiring $83 billion to continue to grow production, as well as $68 billion for farm turnover.

As it eventuated, Australian agriculture ultimately saw an investment of $212 billion in agricultural production over the decade, well above the original forecast. This figure reflected the eventual major inflow of both domestic and global investment into the sector. Despite concerns at the start of the 2010s that attracting investment to Australian agriculture may be challenging, clearly this shows that the momentum of global food demand over the decade, combined with the positive attributes of Australian agriculture, meant that it was ultimately quite achievable.

The coming decade will continue to see structural change in Australian farm ownership as the outlook has shifted substantially from where it may have been five to 10 years ago.

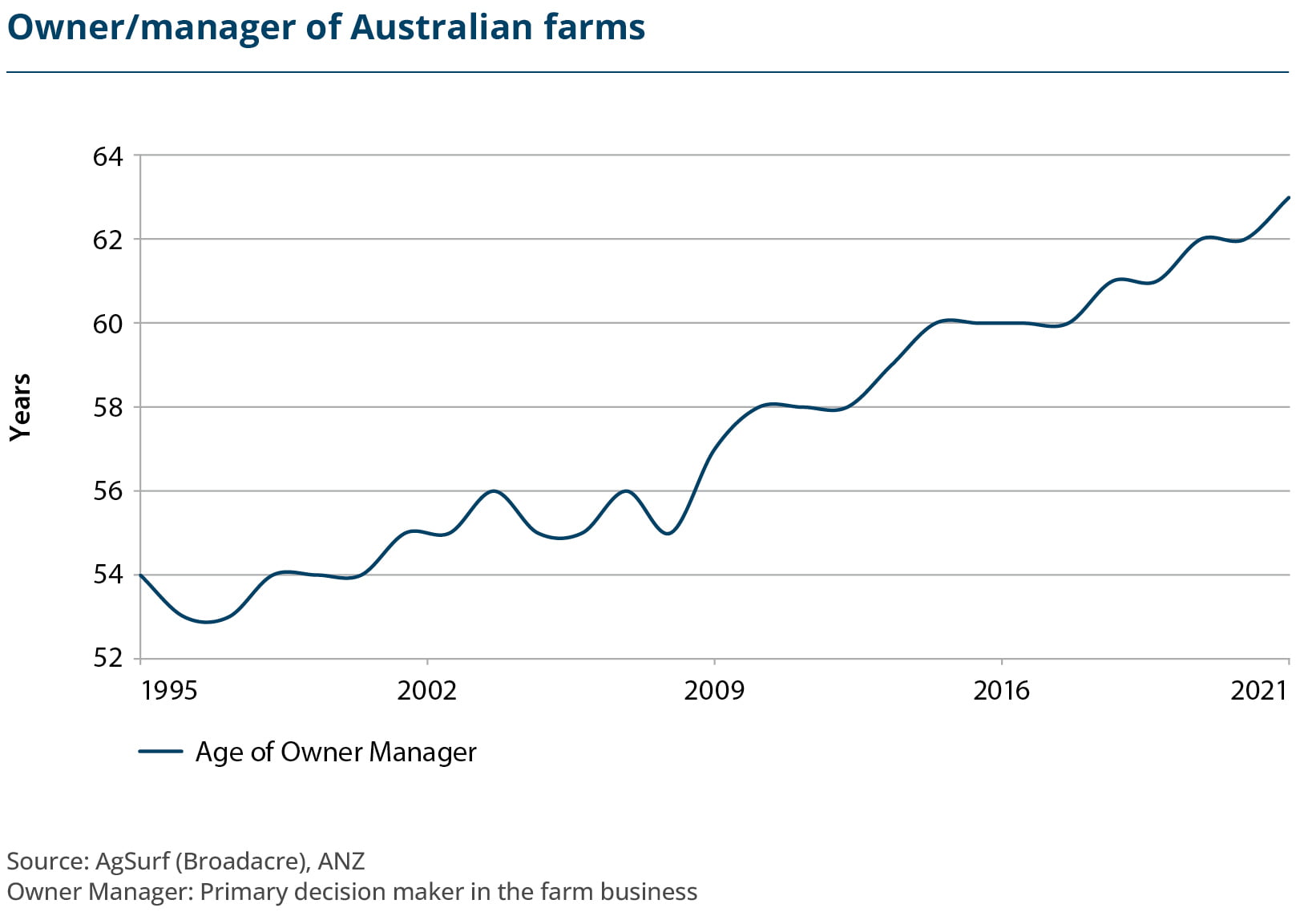

When GP1 was published, it highlighted the average age of Australian farmers as being in their mid-60s. Given the tough conditions for farming at that time, and the potential reluctance of many in the next generation to stay in agriculture, the general outlook was that a large proportion of farmland would likely be purchased by investors and farm management companies would take on the responsibility, and cost, of improving general farming infrastructure and conditions.

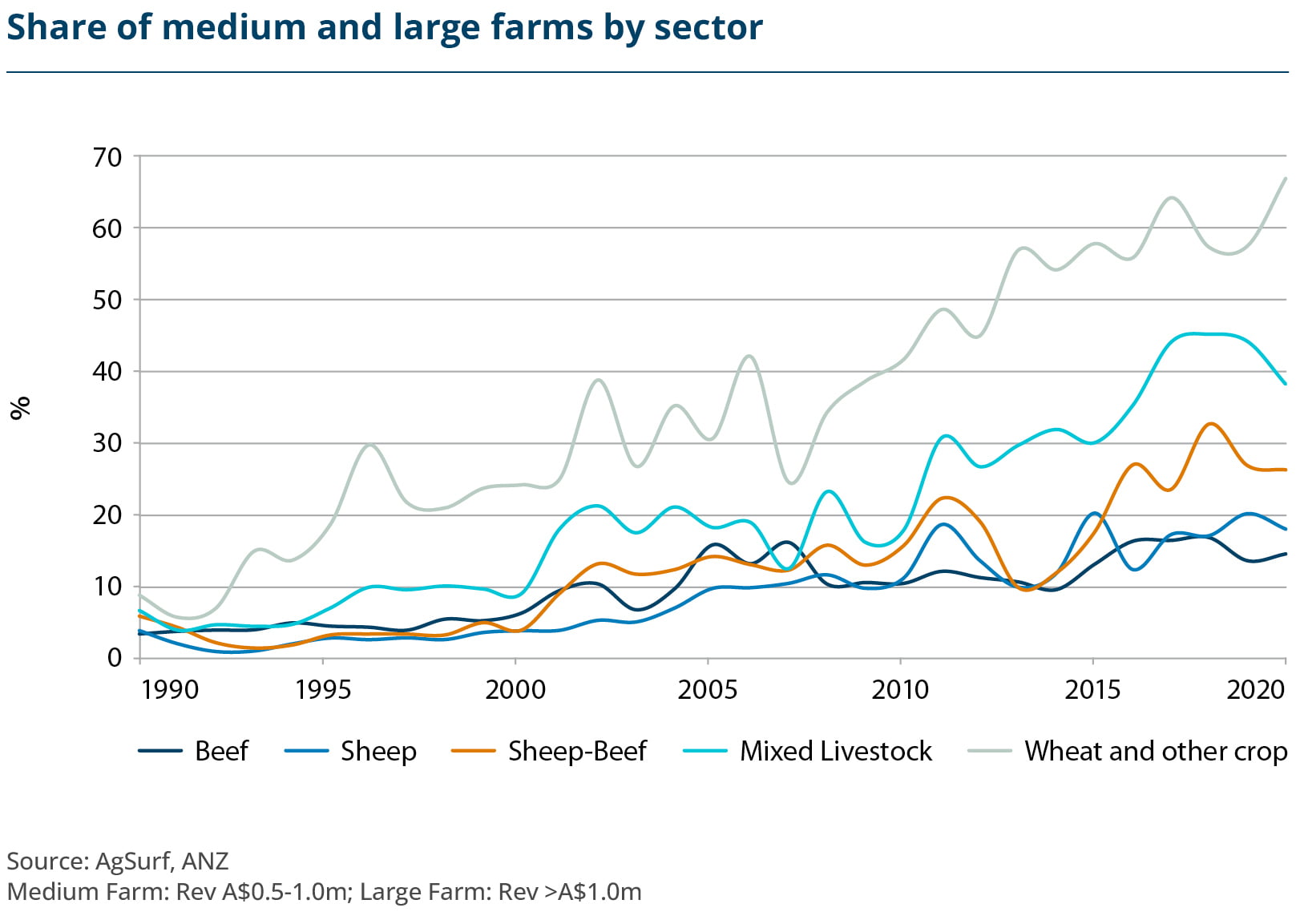

The many positive changes across the agricultural landscape have resulted in this outlook changing considerably. As detailed elsewhere in this publication, the revival of the family farm, with at least two generations working together on one operation, has grown dramatically. Driven by varying factors including sustained high commodity prices and the development of regional centres, farms are now more attractive to family members (and their partners) coming back from capital cities.

The challenge to maintain this momentum now shifts to the future. The decade to 2030 will see an increasing number of variables impacting investment flows into agriculture.

Australian Agriculture has proven to be a compelling investment case for both existing participants and external investors.

These will include changes in global agricultural trade, ongoing consolidation of Australian farms, the increasing impact of agtech implementation, sustainability regulations and climate.

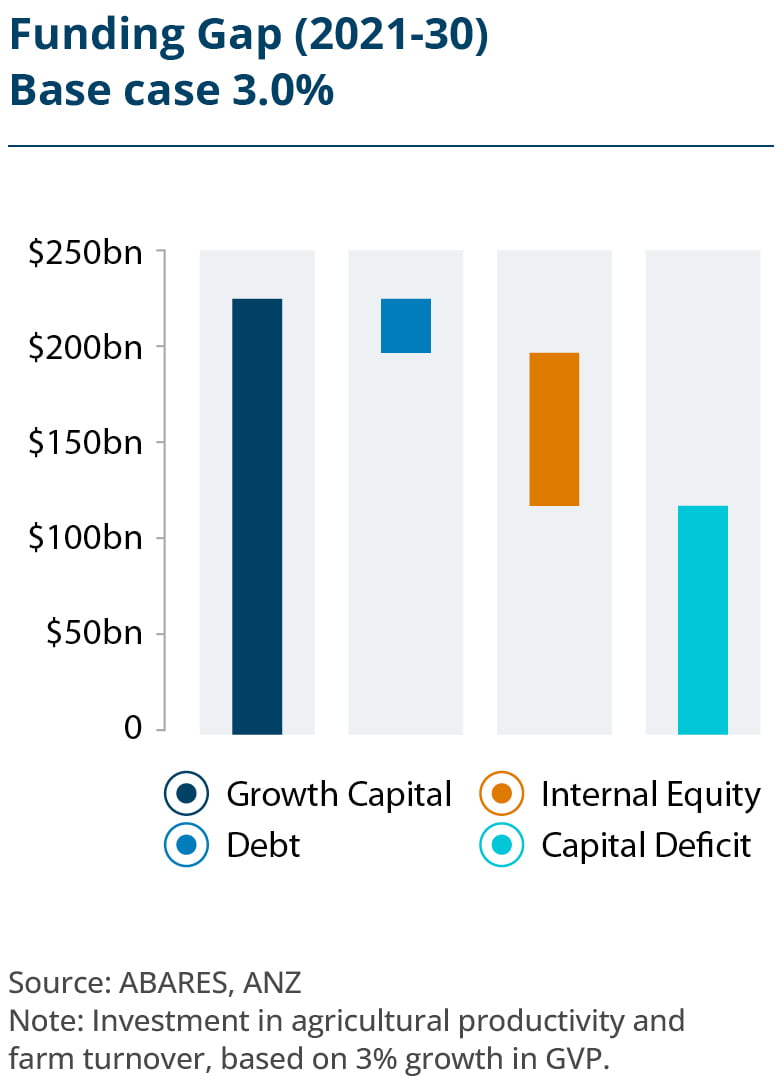

Under the base case forecasts of ANZ modelling over the current decade 2021-2030, Australia will require a further $122 billion in investment to continue to grow agricultural productivity, as well as an additional $118 billion to fund the turnover of farms. These figures are based on Australian agriculture’s GVP climbing from $61 billion in 2020 to $83 billion in 2030.

Given the strong investment growth over the previous decade, this would seem an achievable goal. The challenge will increase if Australia looks to accelerate its rate of productivity.

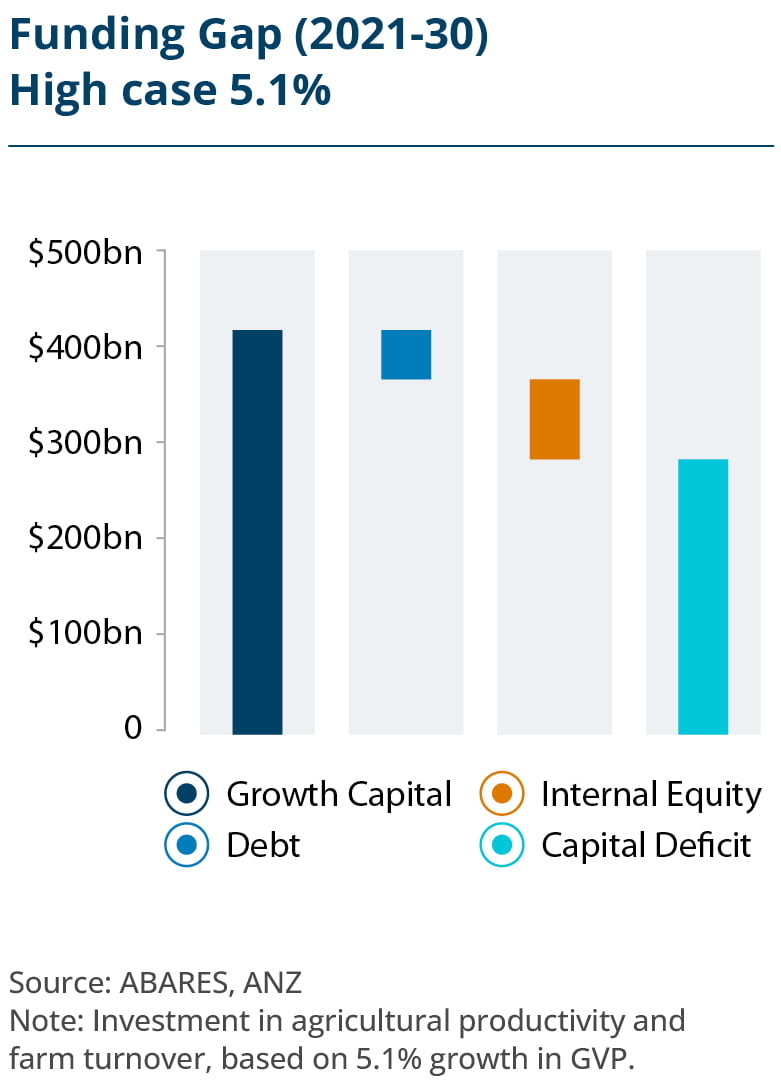

A number of industry stakeholders have called for Australian agriculture to aim for a GVP of $100 billion by 2030. To attain this, production value growth would need to see an annual increase of just over five percent this decade, up from the three percent in the base case. To reach the target of $100 billion GVP by 2030 would require an additional $284 billion in investment for growth, and $133 billion for farm turnover – an increase of 73 percent on the base case requirements, and almost double the level of investment that Australia saw in the 2010s.

Given the variables impacting Australian farms, this report considers that by 2030 Australian farm ownership will be split across the following categories:

Remain in the same ownership

Whether as single generation operations, or family run entities. For many of these, this decade will see them grow in both size and sophistication.

Purchased by either a neighbour, or a local farmer/farming family

The recent sustained run in high commodity prices combined with the positive long-term outlook for the sector indicates strong farmer confidence.

Stay in the same family, but passed on to the next generation

Generational transition may be assisted this decade by factors including high commodity prices allowing older generations access to a new home off the farm, and the growth in regional centres making a move ’into town‘ more attractive.

Purchased and operated by outside investors/farm management companies

While the number of new investors will continue to grow in this type of ownership structure, the growing strength in family farming heightens competition for farm assets.

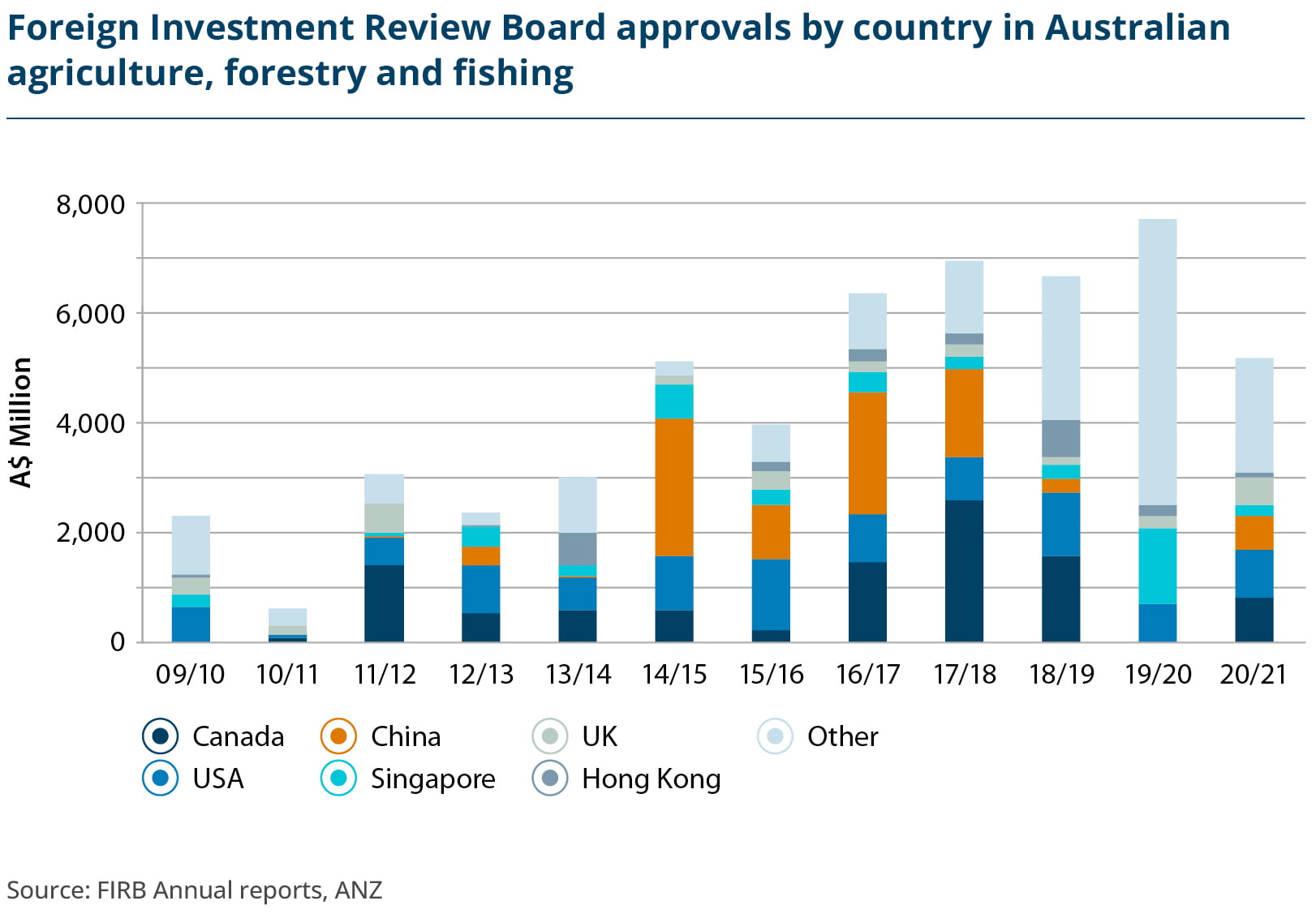

A change in approach towards the origin of investment into agriculture has been a major shift over the past decade.

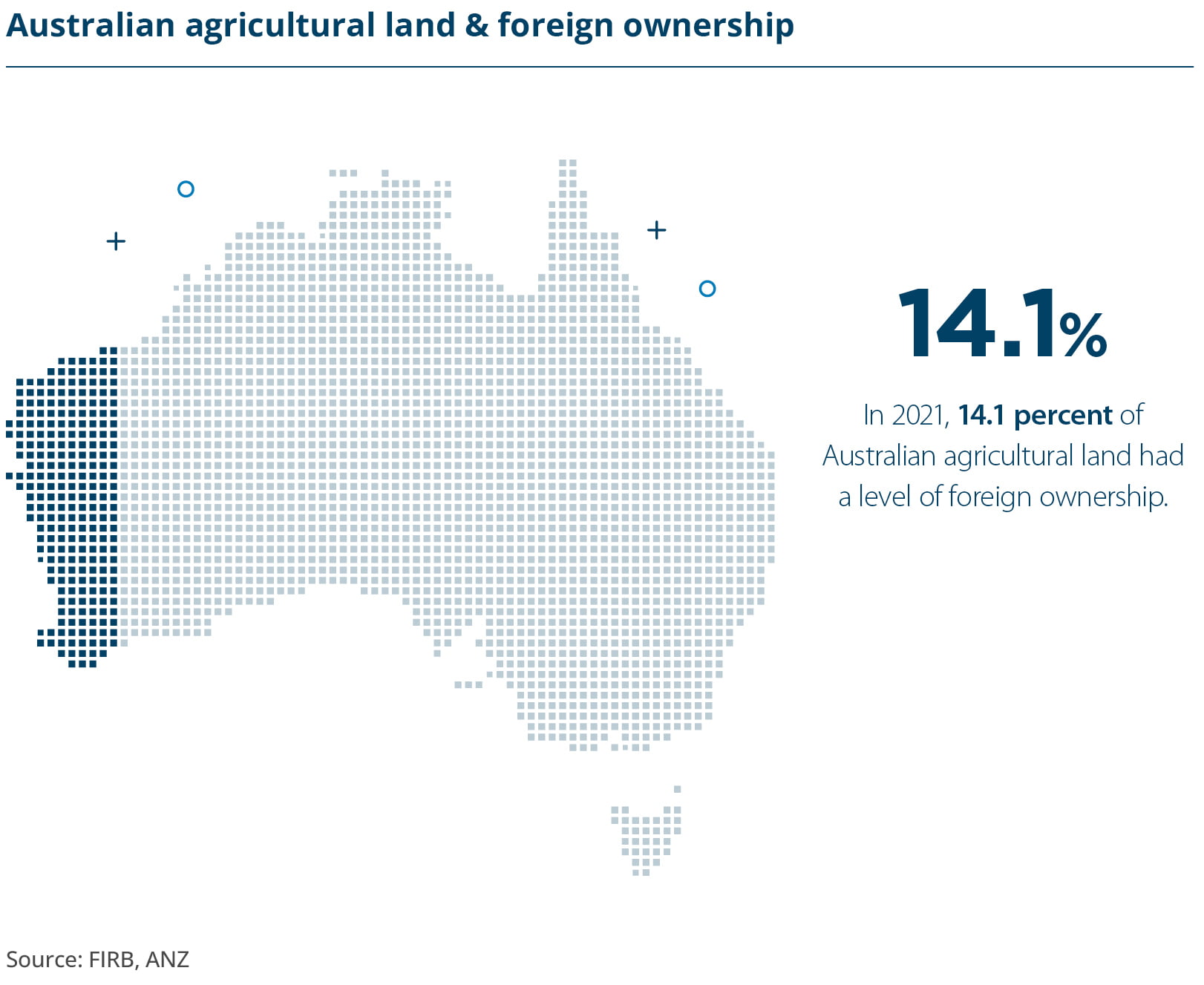

Ten years ago, GP1 highlighted concerns among a number of people in the agricultural and wider communities about both the level and impact of offshore investment into the sector. Offshore investment into Australian agriculture had been a reality for many years – flowing initially from the UK, with more recent examples including the involvement of American investors into the burgeoning Australian cotton sector from the 1960s.

The combination of the growth in global investment capital and the surge in demand for global food imports in the 21st century increased the attention on agricultural production and supply chains as an asset class, with Australia becoming a central focus for investors. In addition to investors from the US, the attention came from Canada, Europe and Asia – particularly China.

The early concerns over the origin of investments were driven by several factors. It was felt by some that foreign ownership of large Australian agricultural production assets may see an increased amount of farm produce diverted to exports, reducing availability or increasing prices for domestic consumers. Another concern was that global agribusinesses could potentially utilise investments in Australian agricultural assets to reduce competition for their operations in other parts of the world, again impacting prices overall.

Domestically, it was argued that Australian investors – and in particular super funds – were being too slow in matching the pace of their global counterparts investing in agriculture. In their defence, the differing approaches and needs of their clients compared to those of their global competitors, made agriculture a sector they needed to approach carefully with a high level of planning and research.

A further change over the past decade, which cannot be underestimated, is the evolution of the capacity by Australian farmers to reinvest in their own sector.

When GP1 was published, one of the main drivers behind the push for new investment into the sector was that Australian producers – the family farmers themselves – would inevitably decline in terms of their role in the wider production landscape, with this space likely to be filled by the growth in corporate farming operations.

Fast forward to the present time where many family farms have emerged stronger than ever and find themselves in a robust position both financially and agronomically.

The Australian family farm has emerged stronger than ever, both financially and agronomically.

This has enabled them to make long term strategic decisions with far more complexity than would have been the case 10 years ago.

Whilst it is difficult to quantify, it is clear across many parts of rural Australia that the approach to scale, succession and generational change has evolved in a positive way.

Not that long ago, many families viewed succession as the departure of the parents and the arrival of the children onto the property. These situations were often quite fraught, tackling issues such as management responsibility handover, as well as the financial restructuring required for parents to move on from the farm.

With the ongoing process of farm consolidation enhancing the scale of many operations, the opportunity increasingly exists for two generations to work together on a farm constructively. The younger generation may return from a tertiary education not only having been trained in agricultural practices, but also possessing new skills, networks, and knowledge of agtech and finance, which positively benefit any farming operation.

The move to more innovative and efficient farming operations ultimately adds to the strength of the overall sector.

That said, multi-generational farming operations can still experience succession issues requiring early attention, including the balancing of relationships between family members of different generations, while ensuring a successful retirement plan for the older generations.

In terms of investment, the reinvigoration of the family farm has allowed this segment of agricultural production to play an increasingly important role.

The ongoing climb in Australian farmland prices is being driven primarily by the stronger family farm sector using their strength to ‘buy the neighbours’ and continue to grow their operations. Not only are they genuinely competing with institutional investors, they are also outbidding them. A family farming operation is more likely to have a multi-generational strategy – rather than a shorter-term return base strategy.

A stronger family farm segment also provides a new investment pathway into agriculture for outside investors.

While still being considered an emerging option, it offers investors who may not have the scale to purchase a major agricultural asset and run a skilled management team an option of partnering with an innovative family operation to jointly build the business.

Importantly, the growth of the family farm brings with it a fundamental, and perhaps unappreciated, boost to the growth and adoption of sustainable farming practices across the Australian agricultural landscape.

Family farming operations are driven by the vision to remain productive for the long term, so that they can be passed on not just to the next generation, but many more to follow. For that reason, family farming operations fundamentally realise the need for climate and production diversity in order to be sustainable well into the future.

Another major change between the 2010s and the 2020s has been in the structure of most large investments into agricultural production. At the start of the last decade, non-farmer investments into large agricultural production assets were predominantly made by corporations or high net worth families or individuals.

Gradually over the last decade, as the profile of Australian agricultural opportunities continued to grow globally, the flow of investments into Australian agriculture grew strongly. These offshore funds included pension funds, endowment funds and family offices and have now reached a point where they are the dominant vehicle for the purchase and management of major agricultural assets.

While this trend looks set to continue, several other factors are likely to strengthen as Australia looks towards 2030.

Forecasts of consolidation across a number of Australia’s superannuation funds will see the emergence of some much larger domestic funds. Given their scale, they will be in a stronger position to invest in larger agricultural production assets.

This is likely to be accompanied by a growth in private investment in agriculture by high-net-worth Australian individuals and families. As the scale of wealth at this end of the spectrum continues to grow dramatically, an increasing number are looking to capitalise on the return potential from agriculture.

The largest family farmers in Australia – keen to capitalise on their successful operations, industry knowledge, and their multi-generational agricultural strategies – are also likely to continue to play a greater role in investing in the sector, contributing to overall industry productivity.