Australia’s Agricultural exports surged beyond expectations

Whilst the value of Australian agricultural production rose strongly in the 2010s, the growth of the sector was largely driven by the unexpectedly strong increase in exports.

When GP1 was published the forecasts for a looming surge in agricultural exports were widely predicted within the industry. The continuing growth of the middle classes – mostly in Asian markets – as well as an accompanying change in diets toward increased consumption of meat and dairy, were highlighted by many as an argument for investing in the sector.

This investment was made to both direct production as well as further down the supply chain, particularly in infrastructure.

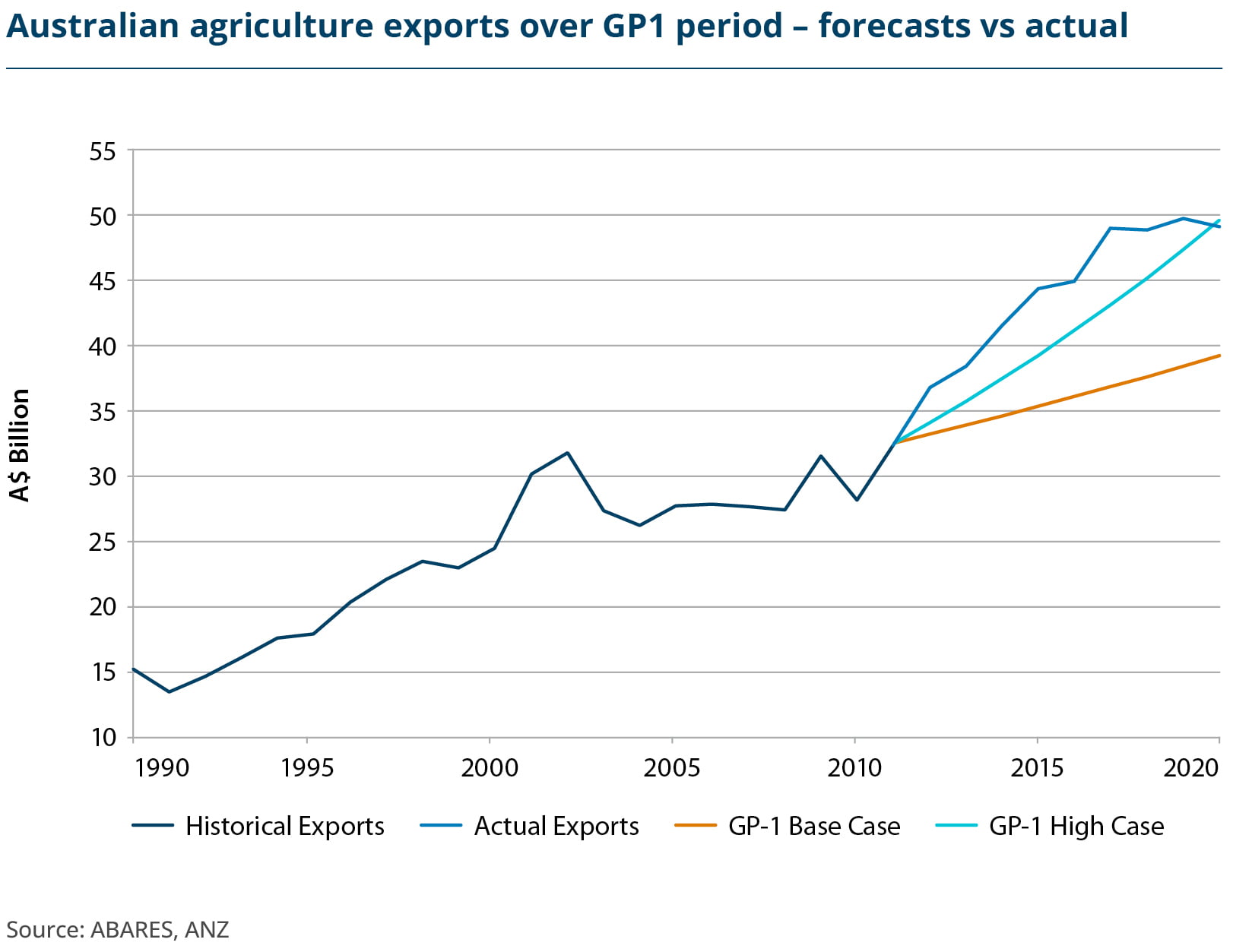

In modelling for the decade 2010–2020, GP1 forecast that Australian agricultural exports would grow strongly above the trend leading into that decade. This ranged from a base case of an extra $33 billion to a high case of an extra $80 billion in exports. GP1 forecast that beef, dairy and wheat were likely to be the commodities in highest demand.

Ultimately, the gains of the decade exceeded even the most optimistic forecast, with Australia recording an additional $111.5 billion of agricultural exports over that period. This growth was principally driven by China’s rapid upsurge in importing Australian beef in the middle of the decade.

Maintaining current trend.

An ambitious estimate based on previous decade’s growth rates.

The forecast that meat exports would increase was largely based on growth trending upwards, rather than the surge which eventuated.

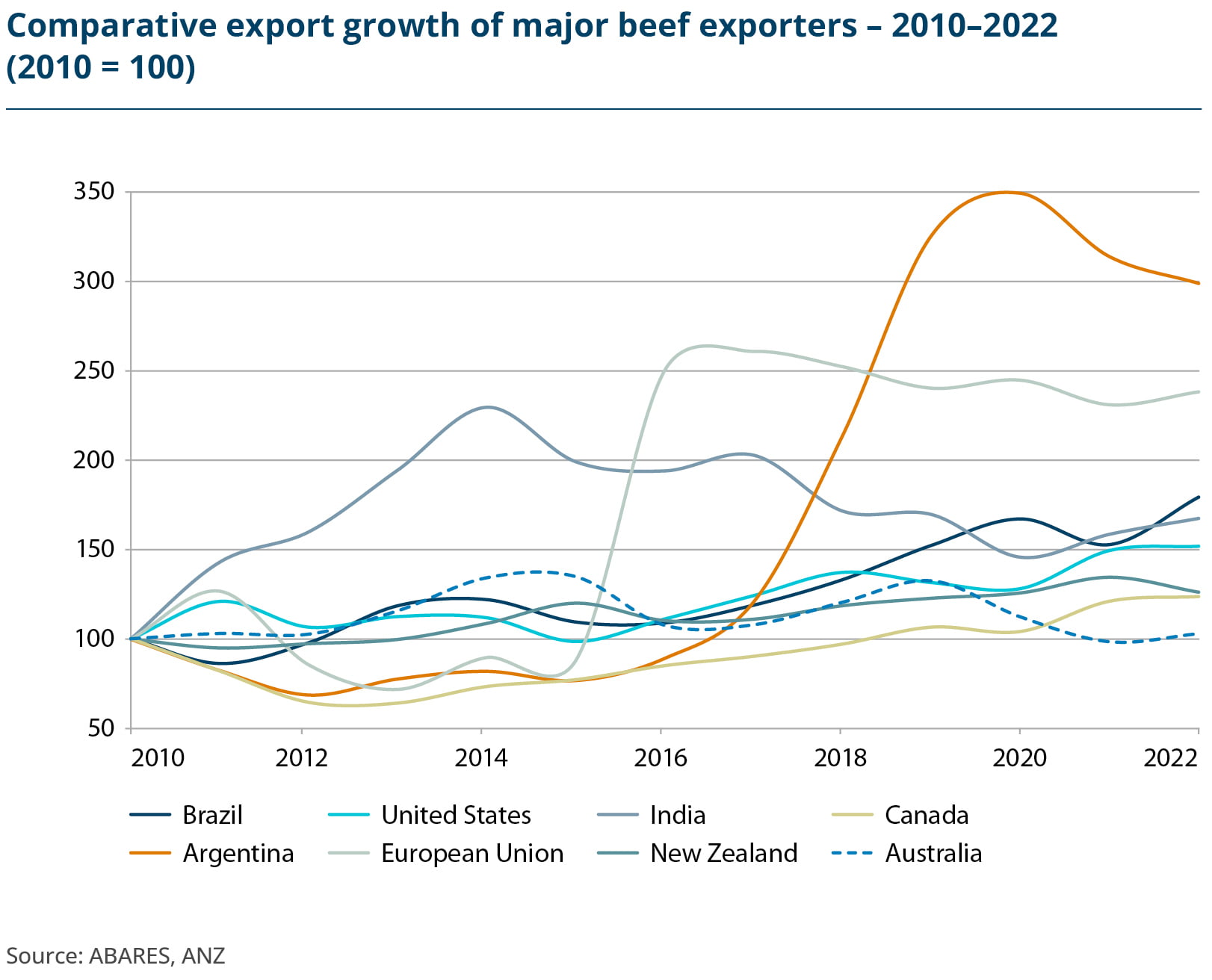

The forecasts were also based on China’s imports coming from a range of markets, including the US and the EU – as it eventuated, Australia accounted for around 33 percent of China’s beef imports in 2015.

Following the initial surge in Australian beef exports to China, Australia’s share of the Chinese beef import market subsequently declined over the remainder of the decade, as China gradually opened up access to other exporters, particularly from South America.

Initially, Australia’s dominant position existed particularly due to favourable perceptions of food safety. When China opened its market to large volume beef imports, most other major beef exporting countries had experienced outbreaks of either Bovine Spongiform Encephalopathy (BSE, or ‘Mad Cow Disease’) or Foot and Mouth Disease (FMD) in previous years.

As a result, they were officially banned from a number of major markets. This included both North and South American exporters, as well as a number of countries in the EU. China, similar to a number of other major Asian markets, was initially hesitant to import beef from markets with any history of outbreaks of this kind. This was particularly pertinent for China, given their major internal food safety crisis around milk and infant formula contaminated with melamine in 2008.

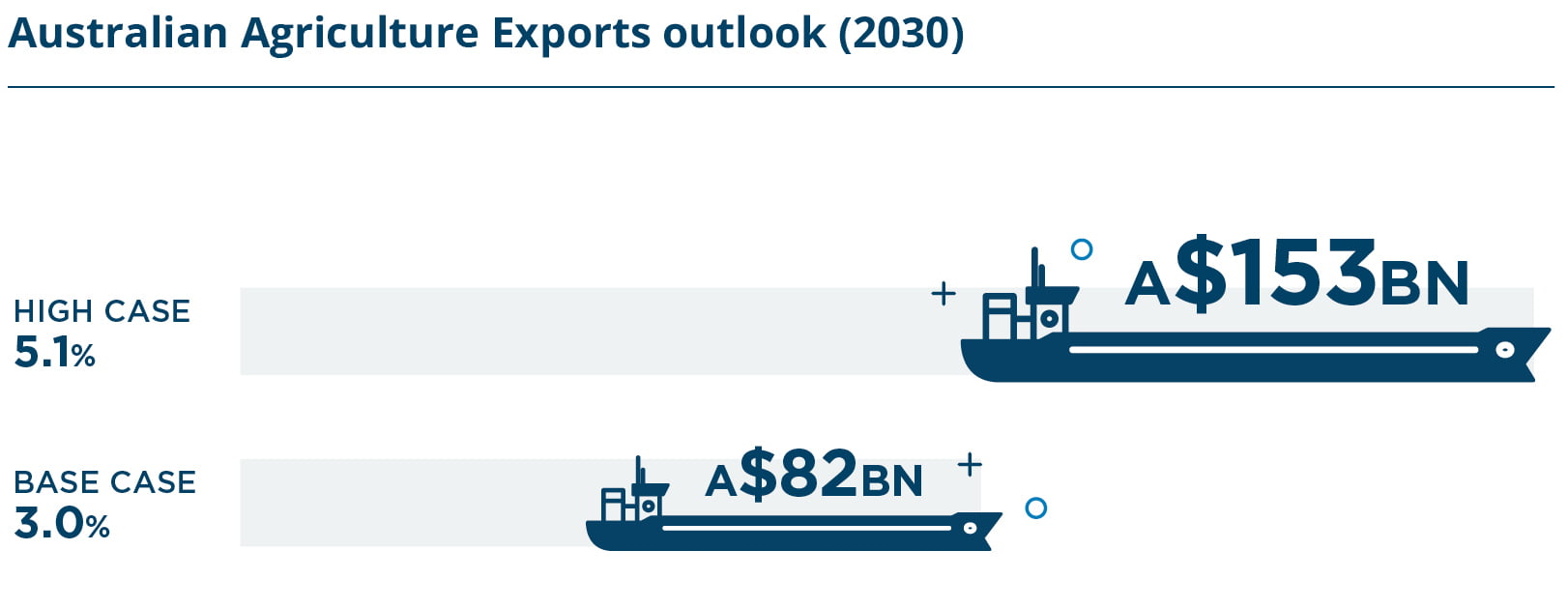

Looking ahead to 2030, ANZ’s modelling suggests that the potential outlook for Australia’s agricultural exports is highly variable. It is a reflection of the previous decade, where unexpected global factors impacted the initial forecasts.

At base trends, with exports rising by three percent per annum, Australian agricultural exports are forecast to gain an extra $82 billion over the next decade, above current figures.

This outlook will change markedly however, if the forecast is based on the high case – particularly if Australia aims to hit $100 billion in agricultural production by 2030. Under this scenario, Australia would gain an extra $153 billion in exports by 2030. This would require a highly ambitious growth rate of just over five percent, but as the events of the previous decade have shown, it has been done before.

Achieving this goal would require strong commodity prices to stay at relatively high levels, though with tightening global food supplies, this assumption seems reasonably likely. In addition, it would also require Australia to not only maintain a major share of its biggest export markets, but also grow its share in other markets. Australia would need to be a leading exporter in a larger number of agricultural commodities, aside from its traditional leaders of wool, beef, and grains. These sectors could include dairy and wine.

To maintain a position as the agricultural exporter of choice to major importers, and continue to demand the price premium which boosts export revenue, Australian agriculture must strive to continue to innovate in commodities. This could include more grains being developed with traits to appeal to particular export markets, or animal proteins produced with lower carbon footprints.