Australian Agriculture’s Gross Value of Production Grew Faster Than Expected

The Gross Value of Production (GVP) receives the most mainstream media coverage of all Australian agriculture economic data.

The GVP is the total price received by Australia’s farmers for all agricultural products when ownership passes from the agricultural production sector, or farmgate, to the next stage, including processing and manufacturing. Examples of this include wool being sold to the processor or fruit being bought by a juice company.

While the GVP is not the only barometer of Australian agricultural growth, it is a very important one. It provides a strong indicator of the economic strength of the farming sector and its ability to innovate and grow. While it is impacted to a degree by changes in commodity prices – when production value and volume trends differ – it also highlights a growth rate for the industry to compare its trajectory against other major agricultural economies.

In 2010/11, Australian agriculture’s GVP was $49 billion. At that time, GP1 forecast that the sector would grow by a base case rate of 2 percent over the decade, rising to $58 billion by 2019/20. This would have meant an overall cumulative gain of $45.5 billion in extra production value over the decade.

In actuality, over that decade, GVP grew stronger than the base case. With an average growth rate of 3.2 percent, the Australian agriculture sector produced $61 billion by 2019/20.

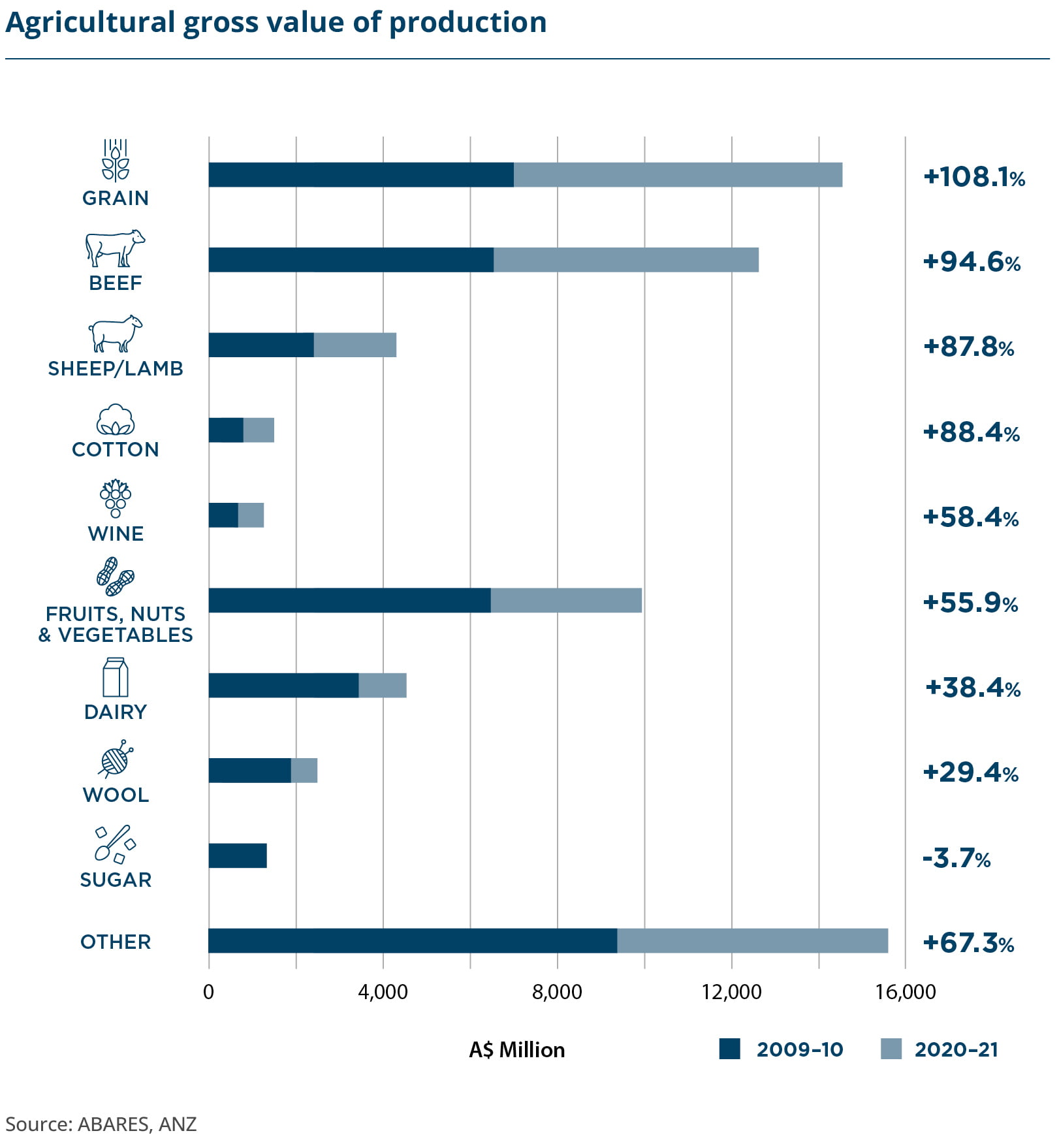

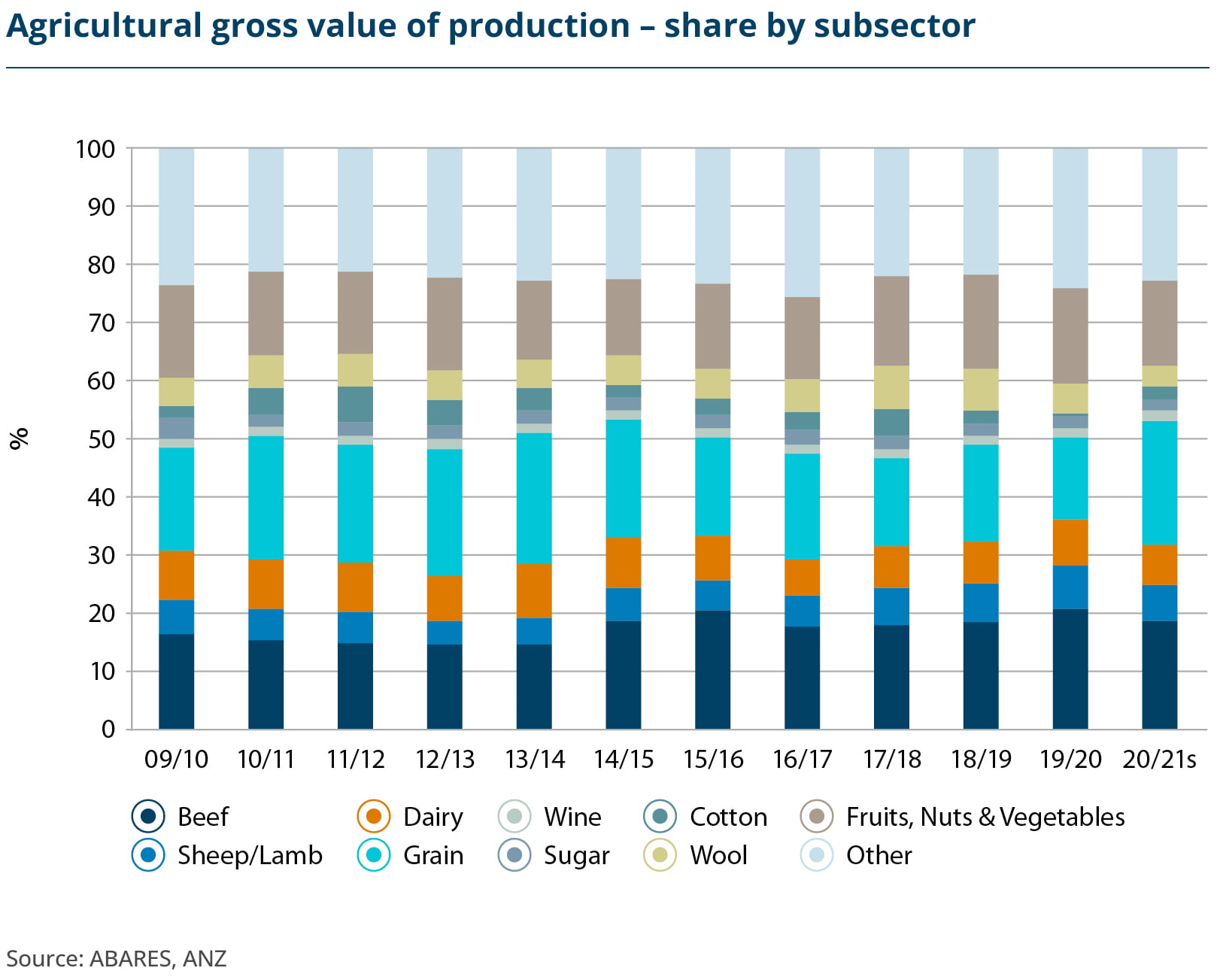

The surge in demand for meat highlighted a clear trend across the last decade as the percentage of Australian agriculture’s GVP for meat overtook that of grain.

Export demand for beef drove up production – in 2019/20 beef production volume reached 2.4 million tonnes (mt) – up from 2.1mt in 2009/10 and doubled in value to $14.6 billion during the same period. This generated higher than forecast prices, with the cumulative gain in GVP over the decade reaching $85 billion – almost double the original forecast.

The strength of beef as Australia’s highest value agricultural product emphasised the importance of developing and maintaining a rigorous biosecurity program. Global consumers increasingly sought beef that was not only of a high quality but also came with a strong food safety record. Australia’s beef was essentially the only large volume product available.

A sustained period of restocking, like the one that followed the drought of 2018/19, is a challenge that may well have a major impact on GVP. Could high prices caused by tight supply compensate for lower volumes, particularly as the restocking program may well be a long one, as producers potentially seek to rebuild their herds well above pre-drought levels?

Unless the global beef industry experiences an unexpected shortage, Australia’s restocking process should eventually bring about a period of notable reduction in supply tightness and an accompanying drop in GVP.

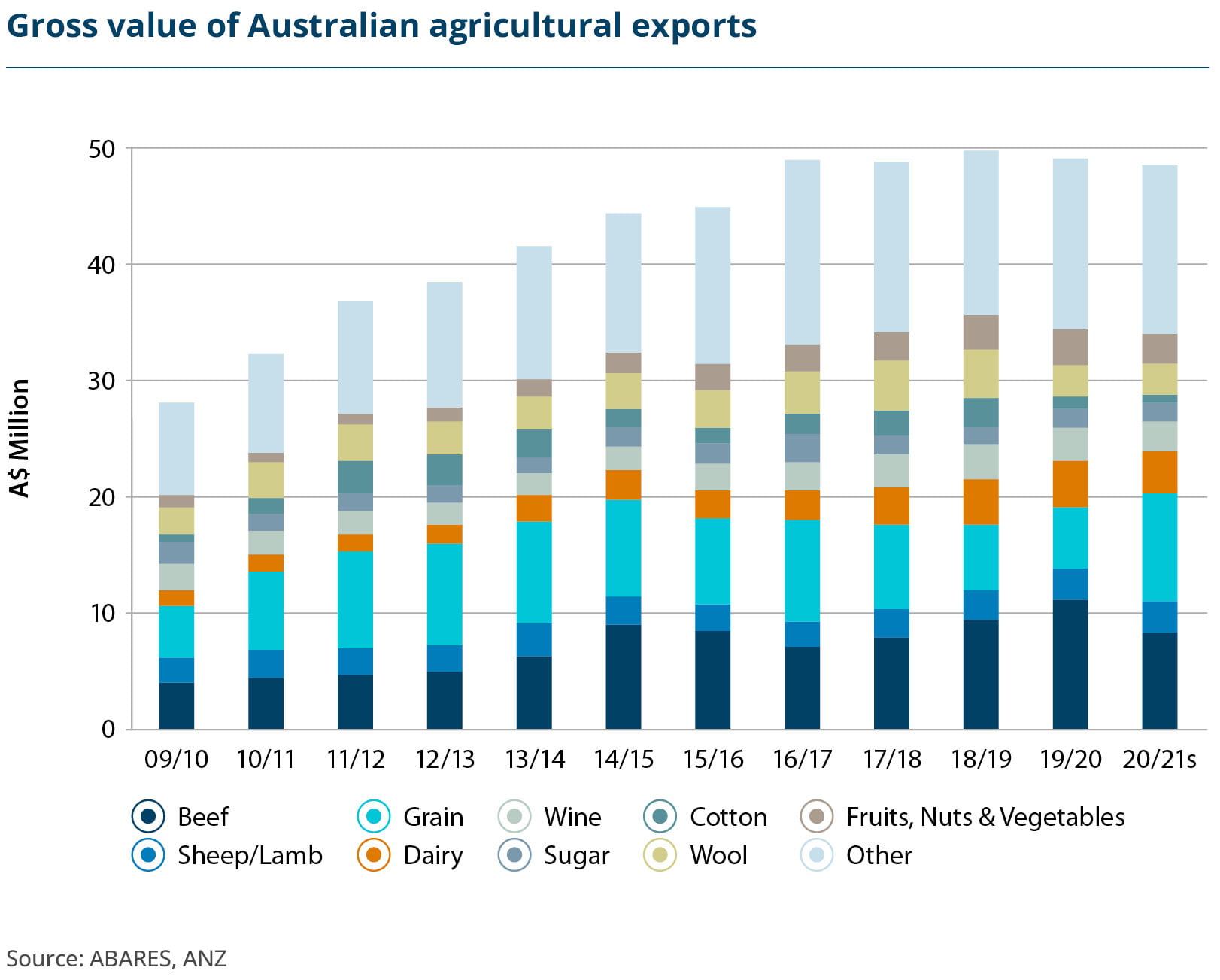

Any ongoing growth in GVP also requires Australian agricultural exports to maintain their reputation for being not just the safest, but of the highest quality. This is reflected in exports including horticulture and lobsters, where Australian products command a premium due to their quality standing.

It is also vital for Australian agricultural producers to continue to develop and refine their product offerings, to ensure that they continue to stand out from major global competitors.

For example, while competitors increasingly improve the quality of their crops, Australian grains are still preferred by many importers due to the innovative focus on grains being grown to suit the specific noodle or bread demands of major markets.

Future GVP calculations may also be impacted if revenues from carbon capture are included in the calculations.