Improve The Trade Landscape

The Australian agricultural sector has been reliant on trade and exports for its prosperity for most of its modern history.

The combination of Australia’s extensive agricultural production area, high quality soils, relatively strong water availability and world leading agricultural production capability, together with a relatively small domestic population and food demand base, are almost unique in global agricultural production – in many ways New Zealand is perhaps the only comparison.

To highlight this, in 2020, Australia’s agricultural exports were valued at $49 billion, out of total agricultural production value of $61 billion.

For the first time in many years, during 2019/20 and 2020/21, agricultural export value declined while agricultural production value increased.

This decline was almost entirely based on a tightness of supply of Australian agricultural products available for export – particularly beef and sheep meat. This was a direct result of farmers restocking after the drought – rather than any reduction in global demand for Australian agricultural products.

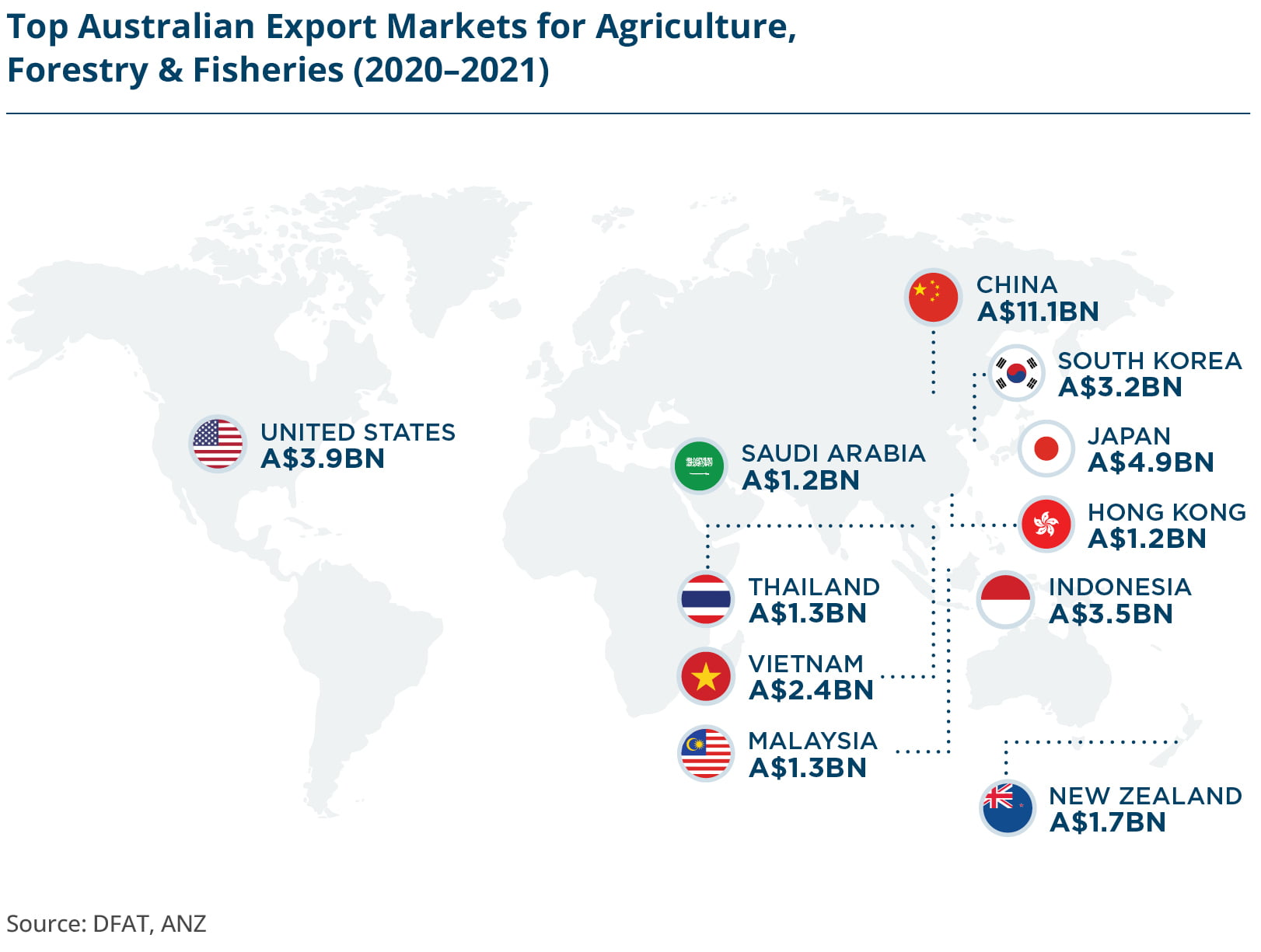

The export strength of Australian agriculture has travelled a long path. The established pattern of working with major export partners began with the United Kingdom as Australia’s major trading partner, and over time extended to include other major partners such as Japan, the US, South Korea and a number of Southeast Asian nations.

The decade leading up to the 2020s was arguably unique. The rise of China as a strong export partner had continued to be discussed but had taken some time to eventuate. In the 2010s, China’s rapid emergence as an importer of Australian agricultural goods – and of those globally – fundamentally changed the export playing field.

As an agricultural trade partner, China’s features are unique. It has a huge population, a middle class with incomes and tastes that continually demand a range of sophisticated foodstuffs, and the capacity to be able to purchase Australia’s premium product offering. Combine these facts with the reality that China – like many other countries – is unable to domestically produce the volume of agriculture to completely feed its own population.

As China’s agricultural import demands escalated over the past decade, Australia emerged as a major trading partner. Australia ticked almost every box required in the relationship – reliability of supply, high product volume, proximity, food safety and quality.

Even while China grew as a trade partner, Australia maintained strong relationships with its existing partners, avoiding a scenario of displacing one market for another.

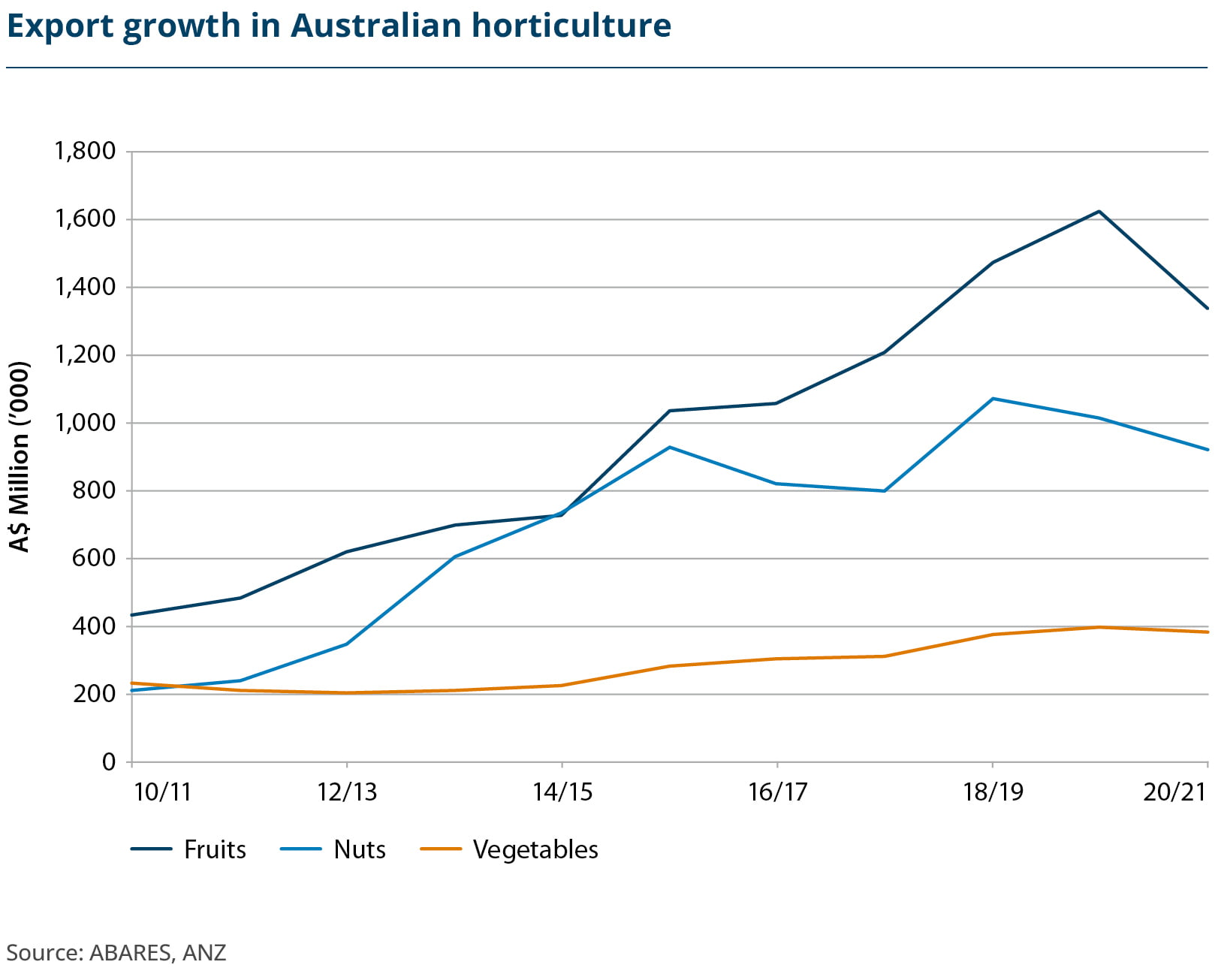

Some Australian agriculture sectors reacted by lifting their production volumes to meet the demand, a trend which both spurred, and was spurred by, a strong growth in new investment. Two strong examples of this were in dairy and horticulture.

At the start of the 2020s, Australia’s agricultural trade landscape with China undeniably experienced some challenges. These situations can be part of almost every major trade relationship, and the resultant challenges allow both partners to develop trade strategies which best position themselves for long term scenario planning and resilience.

For both countries it will be important to maintain constructive dialogue around their agricultural trade relationships, and to consider the most positive long-term outlooks for their populations.

Australia will always be a major player in global agricultural trade. Barring a calamitous event –such as a major biosecurity challenge (which in all likelihood would only impact a particular portion of exports) – Australia will always offer a unique and leading combination of volume, quality and reliability for world agriculture, food and fibre markets.

It is vital for Australia to continue to work hard to enhance its overall trading position and capabilities. Specifically, this will allow the sector to:

become a more resilient global exporter

grow the returns of producers and other supply chain stakeholders

enhance supply chain capabilities

incentivise producers and supply chain stakeholders to adapt

The industry must re-examine its practices at each point, and work to enhance them. This will enable Australia to not only growits reputation as an exporter of choice by product volume and quality, but also improve the ease of doing business.

This will be achieved by maintaining an ongoing focus on areas including trade bureaucracy, quarantine, infrastructure, technology, and payments. Australia must continue to have clear and reliable regulatory settings. This is especially important in promoting investor certainty.

It is vital to enhance all aspects of the quarantine process for exports. All exports of grain, meat, horticulture, and other products need to be free from any phytosanitary issues which may disrupt trade, as well as from any potential concerns in those areas which may be raised.

The ongoing collaboration between industry and government on traceability technologies through the supply chain will further confirm the true legitimacy of many Australian agricultural export products. This will occur against the backdrop of a period where the growing sophistication of counterfeits or substitutes may raise concerns with major importers.

The Australian agriculture export sector has worked hard to build its major trading relationships, and these will always be fundamental to the focus of the sector. Part of this success has been due to the specific concentration and attention on particular trading partners. One example is the long-established presence of offices of Meat and Livestock Australia (MLA) in a number of major markets, continuing to build the relationship of their sector, and complementing the work of Austrade, Australia’s agricultural attaches and others.

This model is reflected in the approach by other global agricultural export competitors of pursuing a detailed export market strategy. The United States Soybean Export Council (USSEC), for example, has a major presence in its markets globally, not just to maintain relationships, but to seek to enhance the product utilisation of its exports.

In addition to continuing to pursue free trade agreements, Australia needs to focus on the evolving changes and needs of its major trade partners, including their consumer needs and import infrastructure. Part of this will involve constantly examining changes in market competition, and how Australia can continue to enhance export product differentiation.

The quest for new markets will always be top of mind for every major agricultural exporter. Australia needs to work with its existing smaller and emerging trading partners to identify their changing needs, as well as partnering to improve their import supply chain capabilities – particularly in the areas of infrastructure and trade technology.

The potential for increased exports to India will grow strongly. India brings its own unique characteristics in terms of specific consumer product demands, as well as the trade-off with its own domestic agricultural production. It is a market which will move quickly, as its middle class grows in similar ways to that of China.

At the same time, Middle Eastern markets are also likely to continue to grow rapidly, particularly in their needs for products like sheep meat, grains and oilseeds. Combined with their relative limitations on domestic agricultural production, these trading partners will not only seek greater imports, but increasingly look to invest right through the supply chain.

In a world of growing and developing global markets that don’t have the capacity for self-sufficiency, Australia’s produce will increasingly be in demand.

Looking ahead to 2030, the global agriculture trading landscape will increasingly be dominated by volume producing countries. The countries of South America, particularly Brazil, will continue to grow their production of beef.

A number of countries and regions, including the EU, Canada and the US will become increasingly larger producers of wheat, other grains and oilseeds.

To remain a strong competitor, Australia must stand out not just in terms of product quality and safety, but in terms of balancing product differentiation with volume.

For example, Australia must continue to refine grain production for evolving customer demands for specific noodle, bread or even animal feed requirements.

In growing horticultural markets, where consumers have specific tastes in everything from citrus fruits to apples and cherries and seek greater volumes of quality fruit and vegetables for a healthy lifestyle, trading partners will look to Australia to be ableto meet these requirements.

While volatile climatic conditions will inevitably impact crops, Australia’s combination of relatively fertile expanses of cropping country, high levels of infrastructure, as well as world-leading grain production management will continue to be a comparative advantage.