Greater Control Of Production Costs Boosted Australia’s International Competitiveness

GP1 highlighted the fact that as costs rose across supply chains, Australian agriculture was losing its international competitiveness.

At that time, costs were high all along supply chains – not just on farms – and this included processing, distribution and exports.

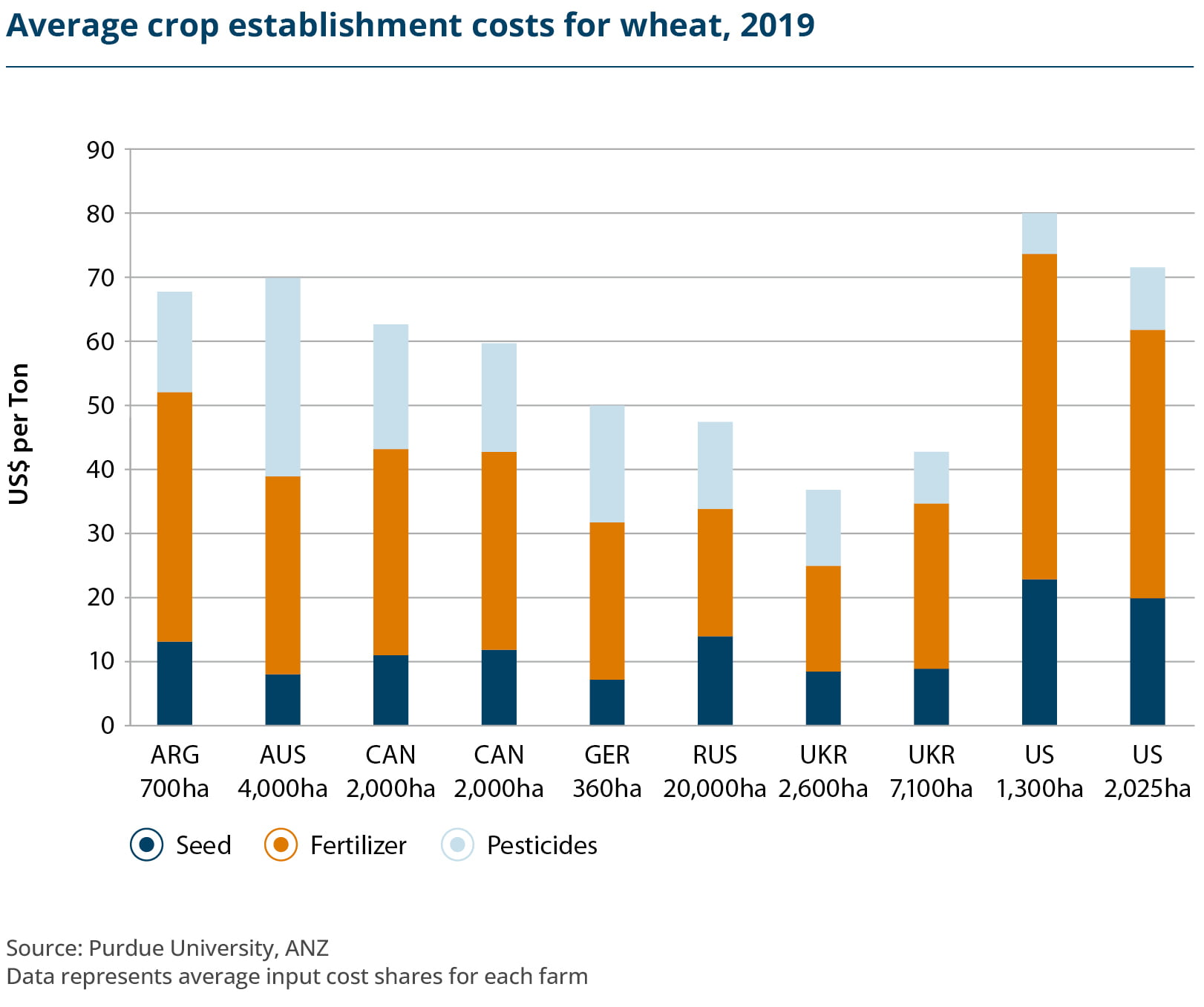

Costs of production are driven by a range of factors, including farm inputs, fuel, plant and equipment, stock feed and labour.

High production costs are a major issue in an unsubsidised agricultural market like Australia, where farmers are unable to fall back on government support schemes if low commodity prices squeeze their operating margins.

Farmers cannot sell their product above a certain price without it being uncompetitive in a global market. High costs of production erode into their margins, reducing the potential for their businesses to grow. This not only impacts their overall production and productivity levels, but acts as a deterrent to investment.

At the same time, when costs are higher further down the supply chain relative to global competitors, it places upward pressure on prices.

As GP1 noted, by the mid–2000s, the average production cost of Australian beef was already double that of Argentina and Uruguay, and about 20 percent more than Brazil.

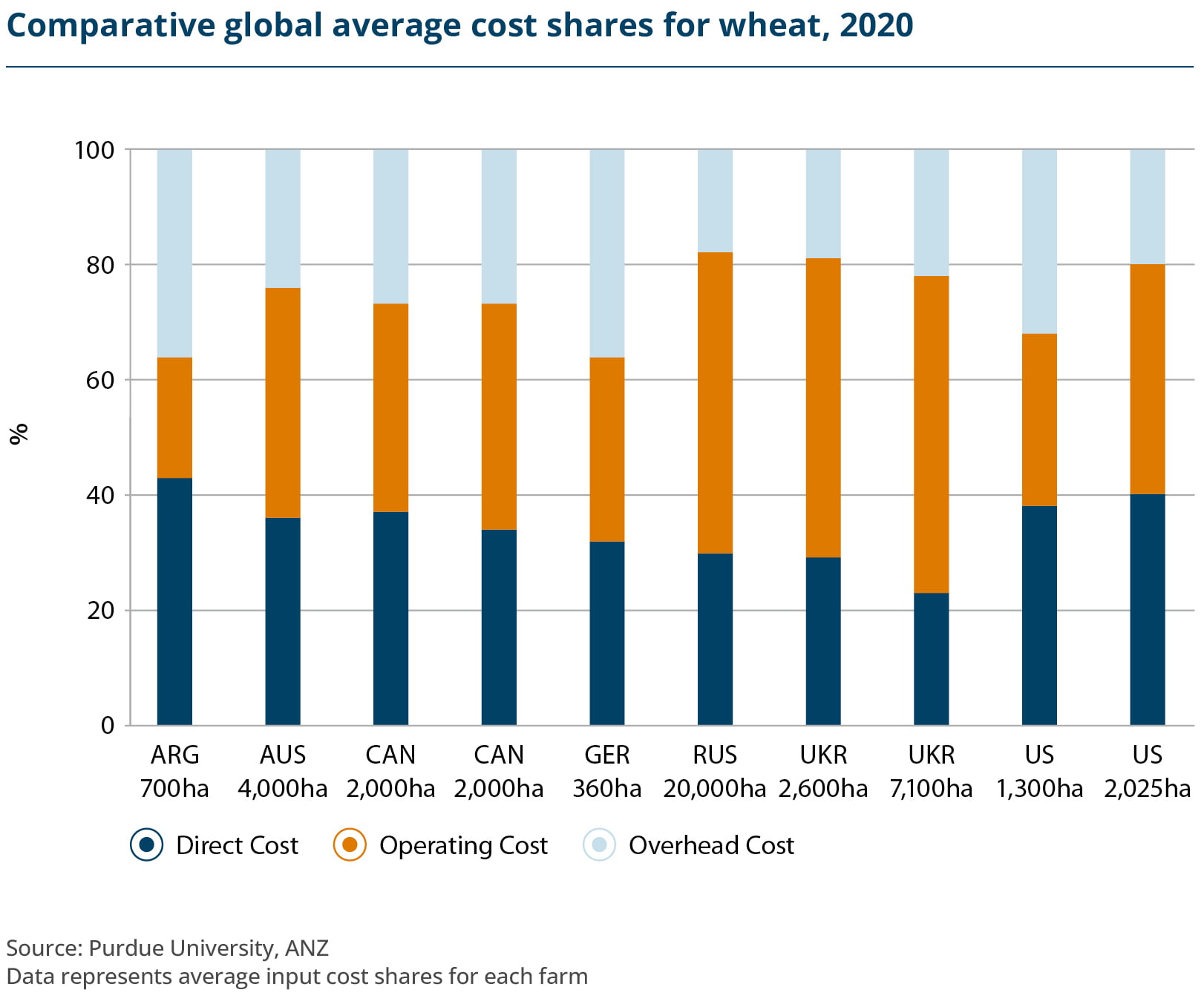

Meanwhile, the production cost of Australian wheat was almost double that of Argentina, and countries in the Black Sea region.

By 2020 however, Australia’s cost of production for most major agricultural products sat comfortably among the best in the developed world. While a factor in the previous decade had often been labour costs, the growth in technology for many agricultural production and processing areas has reduced this as a variable today.

For beef cattle, Australia’s cost structures are now similar to those of North and South America.

Despite this, Australia remains a relatively high-cost producer of wheat. That Australian wheat margins are well above the global average highlights the premium product the industry continues to produce, and arguably justifies the high production costs.

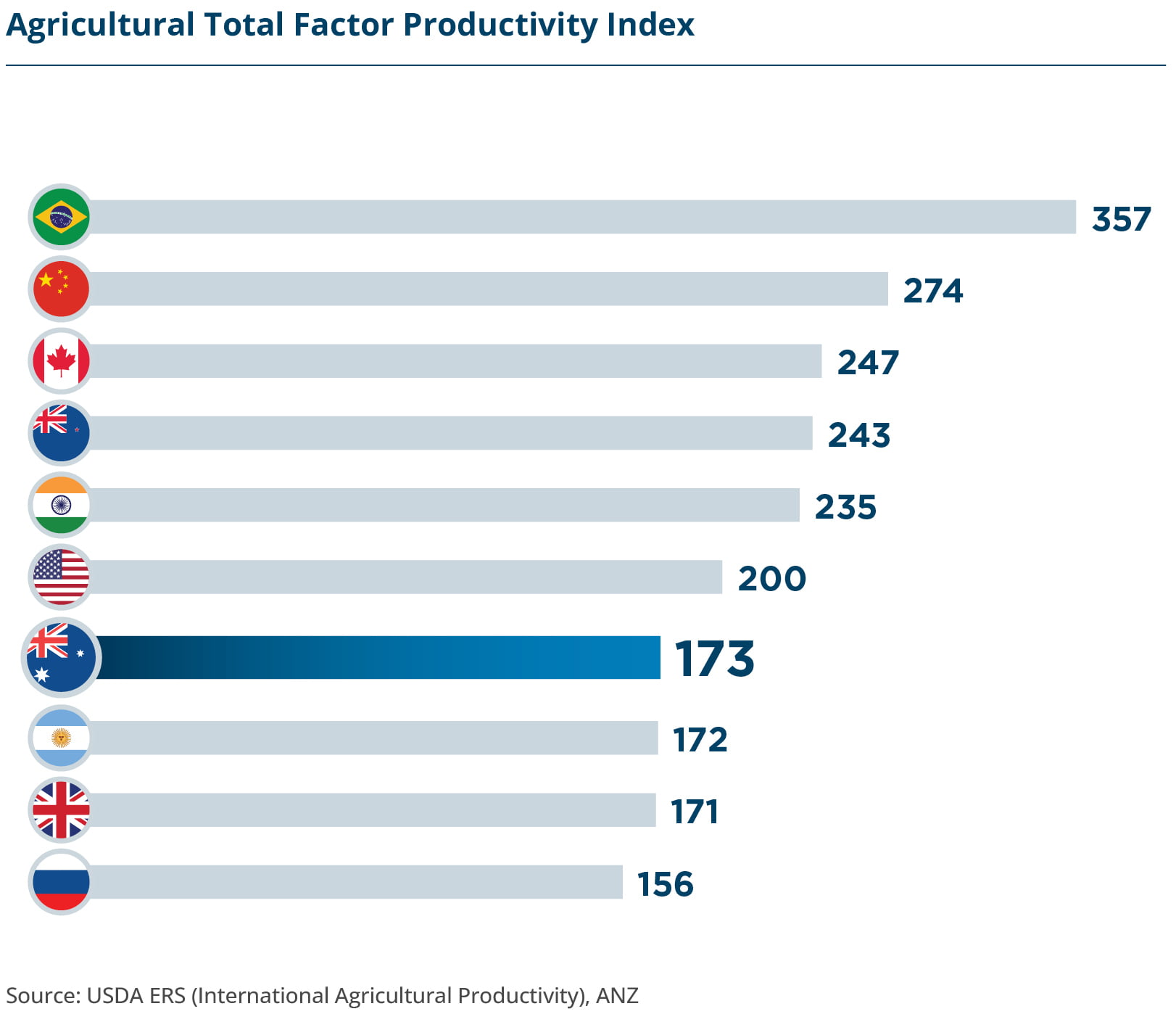

One important indicator of the outlook for Australian agriculture’s future growth and international competitiveness is its Total Factor Productivity (TFP). TFP is measured by taking into account all of the factors involved including land, labour, capital and material resources utilised in farm production, then comparing them with the total amount of crop and livestock output.

Ideally, the output will grow faster than the inputs – leading to positive growth.

Compared to a number of other major agricultural producers, Australia’s rate of TFP has enjoyed strong growth over the past 50 years. Combined with the forecast increased utilisation of agtech, as well as improving levels of efficiency, this growth trend could, and should, continue to rise.

One other factor which stands out from this comparison is the level of volatility in Australian TFP, which is far greater than for any other competitor. This is likely to have been driven predominantly by drought, as well as the absence of smoothing impacts through high government subsidies. In order to reduce the future impact of droughts on TFP, it will be essential for the wider industry to continue to look at measures and strategies for preparing for these inevitable events.

Since 1960, the growth in TFP in agriculture between different countries has varied widely.

Countries which have harnessed research, investment, and structural reform have seen especially strong growth.

Australian agriculture’s TFP growth reflects its start from a higher base, but is also relatively volatile.

Importantly, there is both the potential and the need for TFP to improve.